Waqf: Held Forever, Idle for Centuries, Ready for Activation! How tokenisation operationalises the waqf and unlocks a new source of perpetual, Shariah-compliant capital.

How tokenization operationalizes the waqf and unlocks a new source of perpetual, Shariah-compliant capital.

Imagine a fortune so large that, if it were a country, its economy would rank among the twenty largest in the world. Now imagine that almost none of it has ever been put to work, producing barely anything at all.

That is not a thought experiment. It is the waqf, the Islamic endowment, and it is one of the largest pools of social capital on earth.

We want to walk you through something we believe firmly: this giant can be activated, the way to do it is already proven, and for the first time, the tools finally exist to do it at scale. None of it requires changing what a waqf is.

A trillion dollars, earning less than two percent

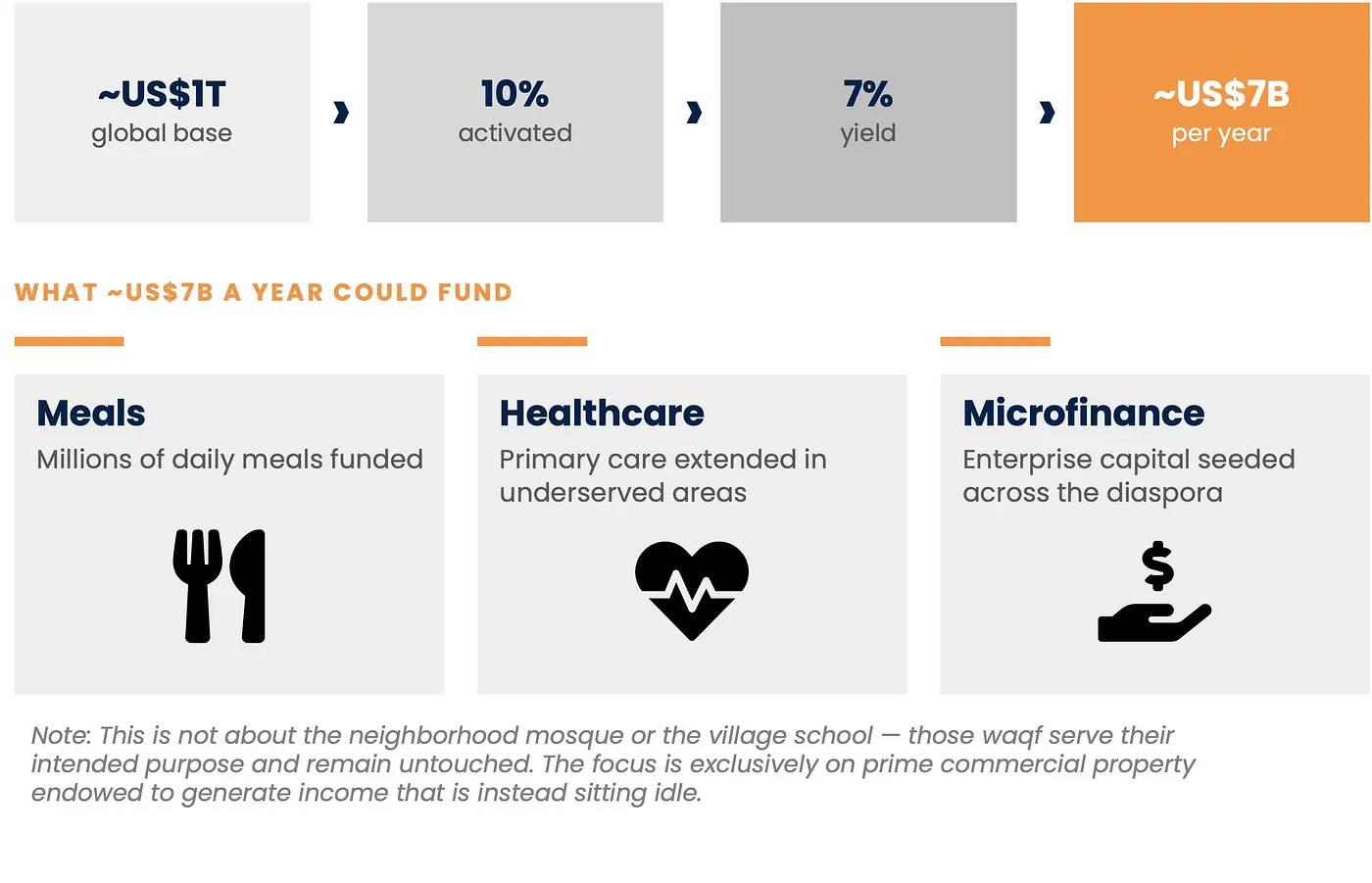

The global pool of waqf assets is worth somewhere around one trillion US dollars. Here is the problem in a single line. That trillion dollars earns less than two percent a year. A professional manager handling that same kind of property would expect five to eight percent. So the sector runs at perhaps a quarter of its potential.

Let us be precise about the diagnosis, because everything follows from it. The money is not missing. The generosity is not missing; Muslims have given for fourteen centuries. What is missing is the financial plumbing, the structures that would let this capital actually go to work.

The arithmetic is simple. We do not need to touch all of it. Activate just ten percent at a sensible seven percent yield, and you generate around seven billion dollars a year in new, recurring income. Every year. In perpetuity.

This is not about the neighborhood mosque, the village school, or the cemetery. Those are waqf doing exactly what they were created to do, and they remain untouched. The opportunity is the prime, commercial-intent property that was endowed to produce income and is instead sitting idle.

And what could seven billion dollars a year do? Millions of meals a day. Primary healthcare for communities that have none. Small-business capital seeded across the Muslim world and the diaspora. This is not abstract finance. It is the difference between an endowment left idle and one that feeds people.

Why now, and not twenty years ago

Across very different legal systems, the same pattern repeats. Indonesia collects barely over one percent of its cash-waqf potential. India’s waqf is among the largest non-government landholders in the country, mostly underused. Saudi Arabia has a documented base of nearly ninety billion dollars and real Vision 2030 momentum. Türkiye runs a centuries-old system that is home to the most ambitious activation attempted yet.

So why now? Three things have changed.

First, the religious questions are settled. The structures rest on classical contracts and the authority of the recognized global standard-setters, AAOIFI and the OIC Fiqh Academy.

Second, the precedents are proven. There are live models with audited results going back two decades, which removes the old fear of execution risk.

Third, the infrastructure has finally caught up. Tokenization, regulated digital assets, and compliant settlement now reach retail donors and cross borders. The idea is ancient. The ability to deliver it at scale is brand new.

So why hasn’t it happened?

If the opportunity is this obvious, the obvious question is why it has not happened already. There are four obstacles, and I want to be honest about all of them.

Title and legal standing. Waqf land often carries an unclear title, and many jurisdictions do not recognize a waqf as a legal person able to hold property, contract, or be financed.

Inalienability. The core asset, the corpus, can never be sold or pledged. That is exactly what makes a waqf permanent, but it also means conventional collateral-based finance does not fit.

Perpetuity. A waqf must endure forever, while most financial vehicles are built to wind up. Few systems bridge waqf law and capital-market law.

Capacity and sponsorship. Trustees are mandated for careful stewardship, not commercial execution, and real reform needs a sponsor with genuine authority.

Here is the single most important point. Not one of these four is a religious prohibition. Classical jurisprudence permits activation. The gap is legal, institutional, and political. And the four reinforce one another in a loop: no clear title, no financing; no financing, no development; no development, no income. The good news about a loop is that once you break it in one place, it can start turning the other way.

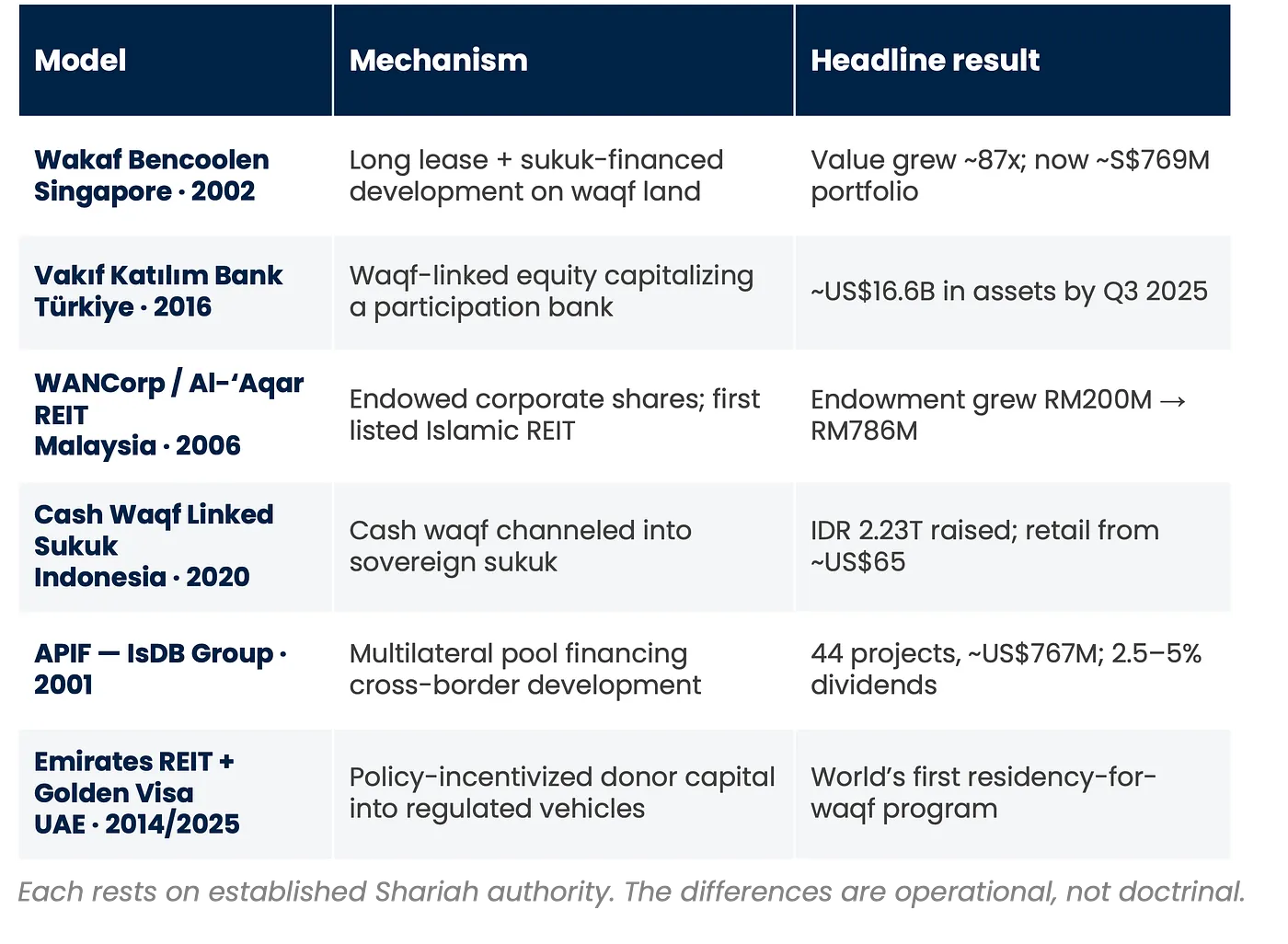

It already works: six live models

The best proof that the loop can be broken is that it already has been. Six different mechanisms operate today across five jurisdictions and one multilateral institution, with audited records reaching back two decades.

Two of them anchor the range.

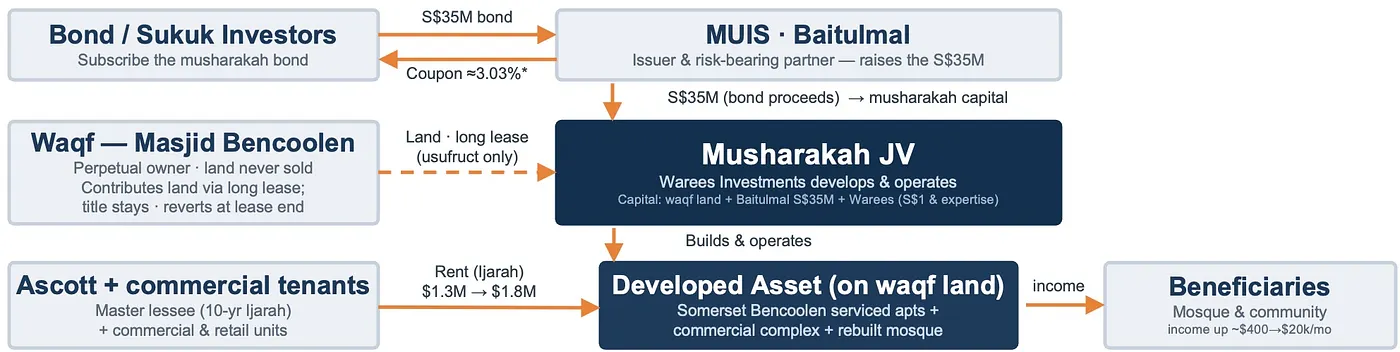

In Singapore, Wakaf Bencoolen took a mosque on extremely valuable central land that, as inalienable waqf, could not be sold or mortgaged. The religious council leased the land long-term to a special-purpose company, which built a mixed-use development funded by a roughly thirty-five million dollar sukuk repaid purely from rent. The title never moved. The endowment’s value grew about eighty-seven fold, to over seventy-one million dollars. The breakthrough was financial, not legal: you finance against future income, never against the asset itself.

In Türkiye, Vakıf Katılım Bank went further. With the Islamic Development Bank as a founding shareholder, a waqf became the equity capital of a licensed participation bank. That bank grew from under five billion dollars in assets in 2019 to around sixteen and a half billion by 2025. It shattered the assumption that waqf has to mean real estate earning rent, lifting the ceiling from property yield to the return on equity of an entire bank. It is the most ambitious model, and candidly the one under the most active Shariah review, but it is operating and regulated.

Six completely different mechanisms, but they share one thing. Every single one rests on established Shariah authority, and activation succeeded by going through the authorities, not around them. The binding constraint today is no longer jurisprudence. It is operational.

The new frontier: the tokenized waqf

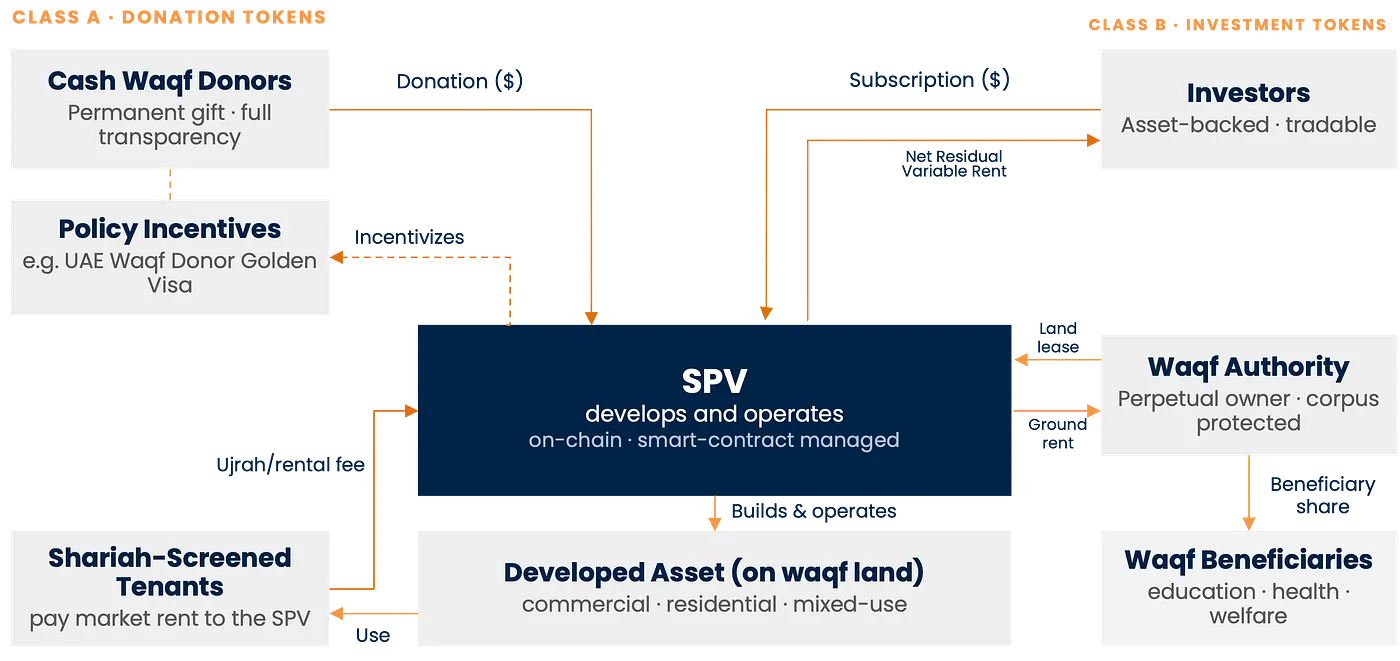

Now the piece that is genuinely new. Let me be clear about what it is and is not. It is not a new religious contract, and it is not a cryptocurrency scheme. It is a digital token layer placed on top of the structures that already work. We are not changing the contract; we are upgrading the plumbing. The land never moves. Only the income does.

Here is how it runs. A waqf authority leases an undeveloped plot, long-term, to a special-purpose company. That company issues two kinds of tokens.

The first, donation tokens (Class A), are permanent gifts. The donor earns no financial return; the token is simply a transparent, verifiable record of exactly what they gave and where it went. It is charity, recorded honestly, and it adds permanently to the endowment.

The second, investment tokens (Class B), are backed by the building and its rental income, not by debt. Because they represent a real claim on a real income-producing asset, they can be bought and sold on a regulated secondary market. Returns are variable and never guaranteed.

With money from both, the company builds and operates an income-producing asset and leases it to Shariah-screened tenants. The rent pays investors a variable return, sends a defined share perpetually to the waqf’s beneficiaries, and at the end of the lease, the entire developed asset reverts to the waqf, which now owns both the land and the building outright.

Throughout, the corpus is never sold, pledged, or exposed to loss; investor risk is ring-fenced inside the company. A Shariah board, on-chain records, and external audit run in parallel, within the host country’s digital-asset and capital-market rules.

That last point about Class B matters most. Liquidity, the simple ability to enter and exit, is exactly what waqf-linked investment has always lacked, and it is the reason people have been reluctant to lock money away forever. Live tokenized sukuk already demonstrate the approach.

Why it changes the economics

None of the advantages below requires bending a single Shariah principle. Each is a property of better infrastructure laid over already-compliant contracts.

Transparency. Every contribution and distribution sits on an auditable ledger, addressing the quiet worry that suppresses giving: where did my money actually go?

Reach and divisibility. Minimums fall to a few dollars, opening waqf to retail donors and the global diaspora.

Cross-border rails. Compliant digital settlement moves a gift across borders in near real time.

Liquidity. A regulated secondary market lets investors enter and exit a once-frozen position.

New corpus through policy. It pairs with innovative sourcing, from residency-for-endowment programs to large structures like the King Abdulaziz Waqf that funds the Zamzam Tower complex near the Grand Mosque, manufacturing entirely new flows of capital.

And the model compounds. Most financial innovation simply grows the return. This grows the endowment itself. Every cycle, the waqf ends up owning more than before.

Activate, do not reinvent

Waqf does not need to be reinvented. It needs to be activated.

The jurisprudence is settled, the precedents work, and the enabling environment has arrived. What now stands between this institution and its potential is no longer permission. It is execution.

A trillion dollars has been waiting, patiently, in perpetuity, to be put to work. The asset base is not gone. It has only been left idle. And activating it is, at last, a choice we are in a position to make.

Disclaimer

The structure solves the financial constraints: it protects inalienability, brings professional capacity, and adds liquidity. What it does not do, by itself, is clear up a disputed title, grant a waqf legal personality, or write the enabling law. Those remain the work of the state and a committed sponsor.

So the model deploys first where that legal groundwork already exists, which is exactly where every live precedent comes from, and it gives reformers a concrete reason to build that groundwork everywhere else. The model solves the financing, not the legislation.